Passive Investing: More Active Than You Think?

The term “passive investing” often conjures an image of effortless, hands-off portfolio management. It implies simply buying broad market indexes and letting the market do the work, with minimal ongoing intervention.

This perception frequently extends to the belief that selecting passive funds is a straightforward, almost trivial task, primarily driven by seeking the lowest expense ratio. However, a deeper dive into how Discretionary Fund Managers (DFMs), like those interviewed by Asset Allocator, approach the task of building portfolios with index-based products reveals a far more nuanced and, indeed, surprisingly active process.

Following up on a previous commitment to explore passive fund selection in more detail, Asset Allocator dedicated time to understanding the intricate methodologies employed by DFMs. While it is true that many allocators strategically build client portfolios heavily weighted with passive funds, largely attracted by their lower cost structures compared to actively managed funds, there’s a critical distinction to be made. Very few of these DFMs would readily admit that their underlying asset allocation itself is passive.

Instead, the prevailing philosophy is that most DFMs adhere to a distinct “house view” – essentially their strategic asset allocation (SAA). This SAA represents their active, informed decision on the optimal long-term mix of asset classes (e.g., equities, bonds, real estate) for a given risk profile. The choice then boils down to how they implement these strategic exposures: either through index funds or through active managers. This immediately introduces an element of active decision-making into the “passive” investment process.

The complexities and challenges associated with selecting an active manager are extensively discussed and well-understood within the investment community. Factors such as manager skill, past performance, investment philosophy, and team stability are rigorously scrutinized. In contrast, the general assumption often is that choosing an index-based product is simple. Yet, as our discussions with DFMs reveal, a considerable amount of effort, research, and due diligence is expended even in creating portfolios comprised primarily of index-based products. This challenges the common misconception that passive investing is entirely passive, particularly at the selection and oversight level.

The Active Side of Passive Selection: Beyond Just Cost

The notion that selecting passive funds is merely a hunt for the lowest expense ratio is a significant oversimplification. As Ben Seager-Scott, Chief Investment Officer at Forvis Mazars, eloquently states, “When managing our portfolio, it takes as much energy overall to manage a portfolio of index-based products as it does active managers.” This statement is striking because it directly contradicts the popular belief that passive management inherently translates to minimal effort. It suggests a sophisticated and detailed approach to passive fund selection, akin to the rigor applied to active manager due diligence.

Seager-Scott elaborated on the multitude of factors that influence his decision-making process for passive funds. While cost certainly remains an important consideration, it is far from the sole determinant. Other critical factors play an equally, if not more, important role:

- Physical Replication vs. Synthetic Replication: This is a fundamental distinction. Physical replication means the fund (typically an ETF or index mutual fund) directly buys the underlying securities in the index it aims to track. This approach offers transparency and generally lower counterparty risk. Synthetic replication, on the other hand, involves using derivatives (like swaps) to mimic the index’s performance, often without holding all the underlying assets. While sometimes cheaper or more efficient for certain markets, synthetic replication introduces counterparty risk (the risk that the swap provider defaults). DFMs like Seager-Scott meticulously assess which method is employed and its implications.

- Securities Lending: Many index funds engage in securities lending, where they lend out their holdings (stocks or bonds) to other institutions for a fee, generating additional income that can offset expenses and improve tracking performance. While beneficial, it also introduces counterparty risk and requires careful oversight of the lending program’s terms and collateral. A DFM needs to understand the fund provider’s policies and risk management around securities lending.

- Tracking Error: This is perhaps the most critical metric for passive funds. Tracking error measures how closely a fund’s performance mirrors its underlying index. A high tracking error indicates that the fund is not doing a good job of replicating the index’s returns, negating the very purpose of passive investing. DFMs spend considerable time analyzing historical tracking error and the factors that contribute to it (e.g., rebalancing costs, sampling methods, fees).

- Capacity and Liquidity: For large allocators, the size and liquidity of the passive fund are crucial. Can the fund absorb significant capital without moving the market or incurring high trading costs? Is there enough liquidity in the underlying securities for efficient replication?

Seager-Scott further emphasized that saving a few basis points on expense ratios is not the primary focus of his research. While he appreciates the ability to “take advantage of competitive market pressures to squeeze prices,” he firmly asserts that he “wouldn’t do it at the cost of long-term returns.” This suggests a balance between cost-efficiency and overall fund quality and performance. He warned that “there are some things that look cheap on the surface, but when you look at some of the underlying costs, it begins to add up.” These “underlying costs” can include hidden expenses related to trading, rebalancing, or the aforementioned securities lending arrangements that might erode returns despite a low stated expense ratio.

He particularly stressed the paramount importance of knowing what you’re buying, especially when dealing with more complex passive funds that track specific strategies beyond broad market capitalization, such as momentum and value strategies. These “smart beta” or factor-based passive funds are designed to capture specific market anomalies. Seager-Scott highlighted a key consideration for such funds: “If you think stocks are going to go from cheap to fair value, and you’re constantly buying the cheaper ones, that can lead to quite high turnover.”

High turnover within a fund, even a passive one, translates to higher trading costs, which eat into returns and reduce the “passivity” of the strategy in terms of underlying activity. This deep level of understanding is far from passive.

The House Selection Approach: Trusting the Provider

For some DFMs, the selection process for passive funds shifts focus from individual products to the fund provider itself. Chris Robinson, Head of MPS at Premier Miton, exemplifies this approach. He estimates his time split for fund selection to be “80 per cent on the active managers and 20 per cent on the passives.” While this still indicates less time on passives than actives, it’s a significant allocation. Crucially, his focus for passives is not on comparing specific ETFs by a few basis points, but on the overall quality and methodology of the fund house.

“When I’m selecting a passive house,” Robinson explained, “I’m usually looking at a team and their instruments of multiple passive solutions that they’re running, because they will run consistent methodologies and approaches.” This perspective emphasizes due diligence on the firm’s operational robustness, its index replication capabilities, its risk management frameworks, and the expertise of its portfolio management teams responsible for the passive suite. The assumption here is that a high-quality fund house will apply consistent best practices across its range of passive offerings.

Robinson’s strategy means he would “tend to sign off on the team and the approach that team uses on an annual basis, rather than specific funds.” This systematic approval process implies that once a DFM trusts a particular passive provider for its integrity, operational excellence, and consistent methodology, they are comfortable using multiple funds from that provider without re-evaluating each individual product in exhaustive detail every time. This approach leverages the fund house’s reputation and scale, recognizing that quality passive management is often about robust internal processes and technological capabilities. It’s a form of active trust in the passive provider.

The “Cheapest Petrol Station” Camp: A Pure Cost Play

In stark contrast to the meticulous, multi-factor approach of Seager-Scott and the house-focused selection of Robinson, there exists a “third camp” of DFMs. These allocators primarily, if not exclusively, buy passives based on cost alone. For them, the selection process is boiled down to a single, easily quantifiable metric: the expense ratio.

James Crocker, Head of MPS at Albert E Sharp, vividly articulated this perspective: “We’d say the art of buying a passive is like the art of finding out which local petrol station is the cheapest.” This analogy humorously, yet pointedly, illustrates a purely commoditized view of passive funds. In this view, one index fund tracking a specific index (e.g., S&P 500) is functionally identical to another, and therefore, the only differentiating factor worth considering is the price. The logic is that if two funds perfectly track the same index, and one charges less, then the cheaper one is always the better choice, as the goal is simply to replicate the market return as efficiently as possible.

This “cheapest petrol station” approach assumes perfect market efficiency and perfect index replication across all providers. It implicitly trusts that minor differences in tracking error, securities lending policies, or replication methodologies are either negligible or are sufficiently priced into the headline expense ratio. While this approach offers undeniable simplicity and cost-efficiency at first glance, it may overlook the subtle complexities highlighted by other DFMs, potentially leading to unforeseen tracking differences or operational risks over the long term. This segment of the DFM community embraces the “passive” nature of passive investing most literally, focusing almost entirely on minimizing explicit costs.

The Nuances of Passive Investment Management

The varied perspectives from different DFMs highlight that “passive investing” is not as monolithic as its name suggests. While the underlying investment strategy aims to replicate a market index rather than beat it, the management and selection of the funds used for this replication are far from inactive.

The industry has seen a proliferation of passive investment products, including traditional index mutual funds, exchange-traded funds (ETFs), and various “smart beta” or factor-based ETFs. Each of these can have different structures, underlying methodologies, and associated risks. For instance, the choice between an accumulating ETF (reinvests dividends) and a distributing ETF (pays out dividends) can have tax implications for different client types.

The use of derivatives in synthetic ETFs introduces counterparty risk that a physically replicated ETF generally avoids. Even within physically replicated funds, there can be differences in how often the fund rebalances to match its index, or whether it uses full replication (holding every security in the index) versus sampling (holding a representative subset of securities), both of which can impact tracking error and trading costs.

Moreover, the regulatory environment surrounding passive funds, particularly ETFs, is constantly evolving. DFMs must stay abreast of these changes, as new rules can impact how funds are structured, marketed, and traded. Operational due diligence on the fund provider – assessing their custodians, administrators, and technological infrastructure – also plays a crucial role. A seemingly cheap fund from a less robust provider could potentially carry hidden operational risks that outweigh the minor cost savings.

Ultimately, the goal of passive investing for DFMs is to deliver market returns effectively and efficiently to their clients. Achieving this goal requires a careful balance of cost control, risk management, and diligent fund selection. It’s about understanding the intricacies of the products chosen and ensuring they align with the client’s investment objectives and the DFM’s strategic asset allocation.

This active oversight of “passive” investments ensures that clients truly benefit from the intended low-cost, market-tracking exposure without encountering unforeseen pitfalls. The conversation around passive investing is evolving beyond a simple “active vs. passive” debate to a more nuanced discussion about “how to implement passive effectively.”

A significant catalyst behind Joby's recent stock surge came with the pivotal announcement of its expanded manufacturing operations. On Read more

The Rolls-Royce (LSE:RR.) share price has demonstrated remarkable vitality throughout 2025, despite experiencing some tariff-induced volatility in April. [caption id="attachment_202" Read more

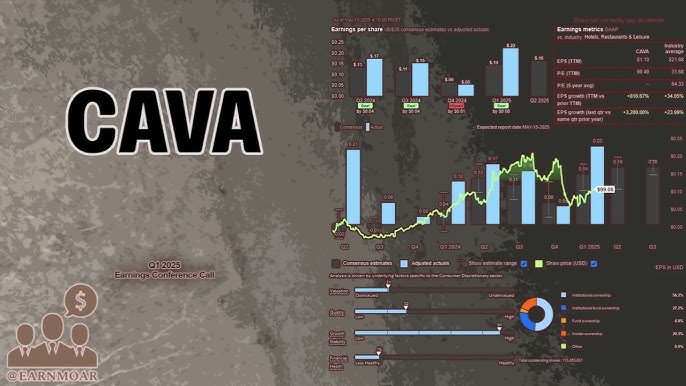

Mediterranean fast-casual restaurant chain Cava has announced impressive financial results for its latest fiscal quarter, concluding on April 20th. [caption Read more

In a significant move poised to reshape its vast entertainment portfolio, Comcast has officially unveiled the name of its new Read more

Taiwan Semiconductor Manufacturing Company (TSMC) is a global titan in the semiconductor industry. Its performance is often seen as a Read more

Tesla Inc. (TSLA) is navigating complex waters regarding the compensation of its CEO, Elon Musk. The company's board of directors Read more