Dimon’s Economic Caution: Navigating US Headwinds

For an extended period now, Jamie Dimon, the influential CEO of JPMorgan Chase, has maintained a remarkably consistent and cautious stance on the U.S. economy. His perspective stands out in a financial landscape often characterized by fluctuating sentiment.

On Tuesday, Dimon reiterated a fundamental truth about economic analysis: accurate forecasts are an immense challenge. He emphasized that true understanding of significant economic shifts often becomes apparent “only in hindsight.” This acknowledgement underscores the inherent difficulty in predicting future market movements and broader economic trends, even for seasoned financial leaders. Dimon’s comments reflect not a lack of confidence, but rather a deep understanding of market complexities and unpredictable global dynamics.

While the long-serving CEO did express a degree of optimism regarding the health of the American consumer, noting their resilience, this positive sentiment was carefully balanced by a series of persistent concerns. He consistently reiterates his worries about specific macroeconomic and geopolitical factors. These include the ongoing impact of tariffs and trade uncertainty, the escalating dangers of worsening geopolitical conditions, the long-term implications of high fiscal deficits, and the potential instability posed by elevated asset prices. Dimon’s viewpoint serves as a crucial counter-narrative to overly optimistic market sentiments, urging vigilance.

The underlying principle guiding JPMorgan Chase, as articulated by Dimon, is a measured approach to making financial projections. He frequently cites past crises that “caught many off guard” as prime examples of why such caution is necessary. These historical events, often characterized by rapid and unforeseen shifts, highlight the limitations of even the most sophisticated predictive models. Dimon’s philosophy is rooted in a pragmatic acceptance of unpredictability.

“Our forecasting of the future is very complex,” he stated directly. “You probably heard me say that sometimes it’s a complete waste of time. Most people cannot really pick inflection points.” This candid assessment from one of the world’s leading bankers underscores the humbling reality of economic prediction: true turning points are rarely visible until after they have occurred, emphasizing the need for robust risk management over precise predictions.

The Broader Challenge of Economic Forecasting

Jamie Dimon’s insights into the difficulty of economic prediction are not isolated; they reflect a broader, systemic challenge facing both policymakers and financial markets globally. The very nature of economic data makes precise forecasting incredibly challenging. Economic indicators are often backward-looking, meaning they provide information about what has already happened, not what is currently unfolding or what will happen next.

Furthermore, this data is frequently revised, sometimes significantly, months after its initial release. These revisions can alter the entire narrative of past economic performance, making it even harder to build accurate forward-looking models based on a constantly shifting historical baseline.

Beyond data limitations, the global economy is increasingly influenced by unpredictable factors that can abruptly “throw even seasoned observers off course.” These include sudden geopolitical events, technological disruptions, natural disasters, and rapid shifts in consumer behavior or policy. Such exogenous shocks are inherently difficult to model and can swiftly invalidate even the most carefully constructed forecasts.

A compelling illustration of this pervasive forecasting difficulty comes from a December study by the Federal Reserve Bank of St. Louis. This comprehensive research examined the Blue Chip Survey of Professional Forecasters, a highly respected compilation that averages projections from approximately 50 leading economists. The study spanned a significant period, from 1993 to 2024, analyzing how accurately these expert forecasts predicted actual GDP growth.

The findings were revealing and somewhat sobering: actual GDP growth came within the forecast range just 44% of the time. This statistic highlights that even a collective of highly skilled economists, utilizing advanced models and extensive data, struggles to consistently hit the mark. It underscores Dimon’s point about the inherent complexity and occasional futility of pinpointing exact economic inflection points. For businesses and investors, this means relying solely on forecasts can be perilous; robust contingency planning and adaptability are often far more valuable.

Dimon’s Consistent Concerns: A Deeper Dive

Jamie Dimon’s recurring cautionary remarks are not arbitrary; they stem from a deep understanding of systemic risks. His consistent focus on several key areas provides valuable insight into the major headwinds he believes the U.S. and global economies face.

Geopolitical Tensions and Trade Uncertainty

One of Dimon’s most frequently cited concerns revolves around geopolitical conditions. The current global landscape is marked by increasing volatility, from regional conflicts to heightened tensions between major powers. Such instability directly impacts global trade routes, supply chains, and investor confidence. When geopolitical conditions worsen, businesses face increased uncertainty, which can lead to reduced investment, supply chain disruptions, and higher operational costs. This can, in turn, depress economic activity and increase the risk of recessions.

Linked closely to geopolitics is the issue of tariffs and trade uncertainty. Protectionist policies, trade disputes, and the imposition of tariffs can disrupt established international trade relationships. For a highly interconnected global economy, these disruptions can lead to higher prices for consumers, reduced corporate profits, and slower economic growth. Businesses struggle to plan and invest when trade rules are constantly changing, fostering an environment of caution and reduced expansion. Dimon often highlights how these uncertainties make long-term planning incredibly difficult for multinational corporations like JPMorgan Chase.

High Fiscal Deficits and Government Spending

Another persistent worry for Dimon is the issue of high fiscal deficits. A fiscal deficit occurs when government spending exceeds its revenue, leading to increased national debt. Dimon frequently points out that the U.S. has been running substantial deficits for an extended period. This unsustainable level of government spending, in his view, poses several long-term risks.

It can lead to higher interest rates as the government borrows more, potentially “crowding out” private investment. High debt levels also limit a government’s ability to respond to future economic downturns or crises, as it has less fiscal space to implement stimulus measures. Furthermore, Dimon worries about the inflationary pressures that can arise from excessive government spending if it outpaces economic productivity, potentially leading to a persistent rise in prices.

Elevated Asset Prices and Market Valuations

Dimon often expresses concern about elevated asset prices, encompassing everything from stock market valuations to real estate prices. While rising asset prices can reflect economic optimism, they can also signal potential bubbles if they become decoupled from underlying economic fundamentals or corporate earnings.

When asset prices become “elevated,” there’s a higher risk of a sharp correction or a market crash. Such events can destroy wealth, reduce consumer confidence, and trigger broader economic downturns. Dimon’s vigilance stems from the historical precedent of market bubbles bursting, leading to significant financial instability and economic pain, something he explicitly references when he states “market valuations and credit spreads seem to reflect a rather benign economic outlook, we continue to be vigilant about potential tail risks.”

The Specter of Inflation

Finally, Dimon has consistently voiced concerns about inflation. While inflation has shown signs of slowing, he has repeatedly warned that it “may persist for some time.” Persistent inflation erodes purchasing power, making goods and services more expensive for consumers and businesses. It can also lead to higher interest rates as central banks try to tame price increases, which can slow economic growth and increase the cost of borrowing for companies and individuals.

For a bank, managing through periods of high and volatile inflation adds layers of complexity to lending, investment, and risk management strategies. Dimon’s early cautions about inflation rising proved prescient, and his continued vigilance suggests he believes the threat is far from over.

Jamie Dimon’s Public Economic Commentary: A Timeline

A review of Jamie Dimon’s public comments over the past quarters reveals a pattern of consistent caution blended with an acknowledgment of the U.S. economy’s remarkable resilience. His statements provide a chronological narrative of his evolving perspective on key economic indicators and geopolitical shifts.

April 2024: “Unbelievable” Consumer Strength Amidst Potential Recession

In April 2024, Dimon made a notable comment that highlighted a paradoxical strength within the U.S. economy. Speaking at an event, he described the American economic boom as “unbelievable.” This positive observation reflected the robust performance and surprising durability observed at that time. However, even amidst this optimism, Dimon maintained his characteristic caution regarding the broader economic trajectory. He quickly qualified his positive assessment by stating,

“Even if we go into recession, the consumer’s still in good shape.” This distinction is crucial. It suggests that while macro-level indicators might point to a potential downturn, the fundamental financial health of the average American consumer – characterized by relatively strong balance sheets and employment – could serve as a buffer, potentially making any recession less severe or prolonged than historical examples. His focus on consumer health underscores its critical role in driving economic activity and providing a foundation of stability.

July 2024: Vigilance Against “Tail Risks”

By July 2024, Dimon’s commentary began to explicitly highlight growing discrepancies between market perceptions and underlying risks. He observed, “While market valuations and credit spreads seem to reflect a rather benign economic outlook, we continue to be vigilant about potential tail risks.” This statement is significant. “Benign economic outlook” implies that financial markets, particularly in terms of stock prices and the cost of borrowing (credit spreads), were pricing in a smooth and favorable economic path.

However, Dimon was actively looking beyond this surface-level optimism. “Tail risks” refer to unlikely but potentially catastrophic events that, if they occur, could have severe consequences. He specifically cited factors that could trigger such events, including escalating geopolitical risks, the ever-present concern of large fiscal deficits, and other compounding factors that could destabilize the seemingly calm market. His message was clear: complacency in financial markets could lead to being unprepared for unexpected shocks.

October 2024: Persistent Issues Beyond Inflation Slowdown

In October 2024, Dimon acknowledged some positive developments in the economic landscape but quickly pivoted to his lingering concerns. He stated, “While inflation is slowing and the U.S. economy remains resilient, several critical issues remain.” This perfectly encapsulates his balanced yet cautious view. He recognized the progress in taming inflation, which had been a significant worry for policymakers and consumers alike.

He also noted the continued resilience of the U.S. economy, which had consistently defied predictions of a rapid slowdown. However, this acknowledgment of positive trends did not diminish his deep-seated concerns. He once again pointed to “large fiscal deficits,” emphasizing their long-term unsustainability. He also brought attention to “infrastructure needs,” highlighting the necessity of significant investment to maintain competitiveness. Critically, he warned about the “restructuring of trade” and the ongoing “remilitarization of the world,” both of which suggest a fundamental shift in global economic and political order that could have profound, unpredictable consequences.

January 2025: Business Optimism vs. Structural Warnings

Most recently, in January 2025, Dimon offered a glimpse into business sentiment while maintaining his foundational warnings. He observed that “Businesses are more optimistic about the economy, and they are encouraged by expectations for a more pro-growth agenda and improved collaboration between government and business.” This indicates a positive shift in corporate confidence, perhaps fueled by anticipation of supportive policy environments and a desire for greater private-sector engagement with government. This optimism could translate into increased investment and hiring.

However, Dimon immediately tempered this positive outlook by repeating his warnings about “government spending and geopolitical risks.” This reiterates his consistent view that despite any short-term optimism or policy shifts, underlying structural issues and external threats continue to pose significant dangers. He also added another crucial point: “Inflation may persist for some time.” This indicates his belief that despite some recent moderation, inflationary pressures could remain a lingering challenge, impacting consumer purchasing power and corporate profit margins for the foreseeable future.

Implications for Businesses and Policymakers

Jamie Dimon’s consistent and publicly articulated caution carries significant implications for both businesses and policymakers navigating the current economic climate. For businesses, his warnings serve as a powerful reminder of the need for prudent financial management and strategic flexibility. Companies are encouraged to maintain healthy balance sheets, manage debt levels carefully, and avoid overextending themselves based solely on short-term market euphoria.

The emphasis on geopolitical and trade uncertainties suggests that businesses should diversify supply chains, re-evaluate global dependencies, and build resilience against unexpected disruptions. Investing in robust risk management frameworks becomes paramount, allowing companies to anticipate and mitigate potential shocks rather than simply reacting to them. Dimon’s outlook suggests that while growth opportunities exist, they are increasingly accompanied by complex, interconnected risks that demand sophisticated navigation.

For policymakers, Dimon’s comments underscore the urgency of addressing underlying structural issues. His repeated warnings about high fiscal deficits highlight the need for sustainable long-term fiscal planning, potentially involving difficult decisions regarding government spending and taxation. His emphasis on geopolitical risks calls for nuanced foreign policy strategies that prioritize stability and predictable international relations, crucial for global economic interconnectedness.

Furthermore, his caution on persistent inflation means central banks and governments must remain vigilant, potentially needing to continue with tighter monetary policies or exploring supply-side reforms to alleviate price pressures without stifling growth. Dimon’s message to policymakers is clear: while short-term economic data might offer comfort, ignoring long-term structural vulnerabilities and external threats could lead to significant and challenging consequences down the line. His insights encourage a proactive, rather than reactive, approach to economic governance.

Jamie Dimon’s sustained cautionary stance on the U.S. economy is not merely a pessimistic outlook but a calculated perspective rooted in historical lessons and an awareness of complex global dynamics. His ability to articulate these concerns consistently, even when market sentiment shifts, provides valuable guidance for anyone seeking to understand the true state of the economy and prepare for potential future challenges. His voice continues to be a critical one in the ongoing economic dialogue, reminding us that prudence and vigilance are always wise investments.

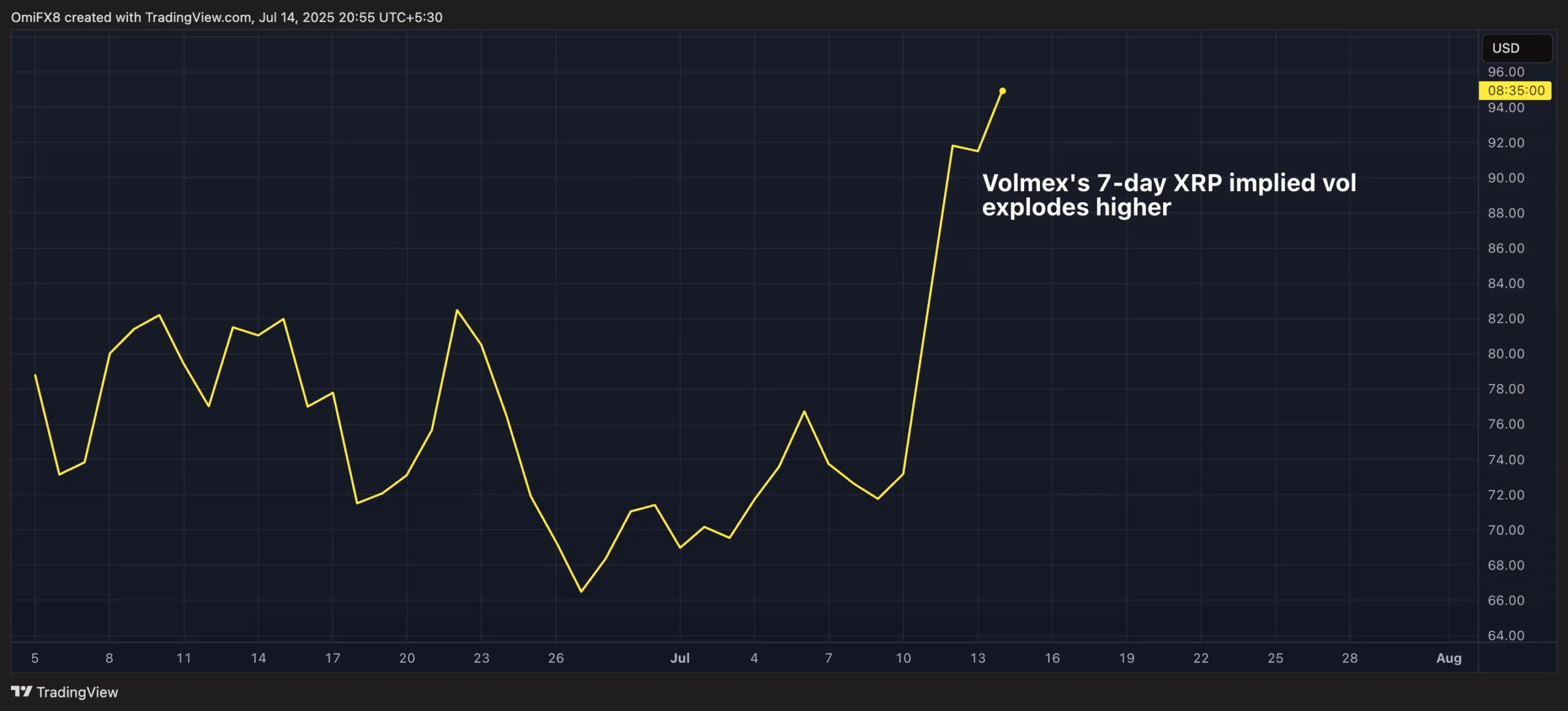

The cryptocurrency market is buzzing, and all eyes are currently fixed on XRP. This digital asset is exhibiting a remarkable Read more

The Rolls-Royce (LSE:RR.) share price has demonstrated remarkable vitality throughout 2025, despite experiencing some tariff-induced volatility in April. [caption id="attachment_202" Read more

Taiwan Semiconductor Manufacturing Company (TSMC) is a global titan in the semiconductor industry. Its performance is often seen as a Read more

Sending a letter or a postcard in the United States just became a little more expensive. The United States Postal Read more

CoreWeave, the specialized cloud provider backed by Nvidia and focused on AI infrastructure, saw its stock price decline by over Read more

Understanding a company's financial health and growth trajectory requires a look at its core operations. While share price movements capture Read more